As we move into 2026 Colorado’s homeowners insurance market continues to reflect long term pressure rather than a short-lived correction. Homeowners across the state are now paying some of the highest premiums in the country with average annual costs pushing past $4,100 which represents roughly a 130% increase over the last decade. At the same time non-renewals and cancellation notices have surged. From 2018 through 2023 Colorado experienced an estimated 77% increase in homeowners insurance non-renewals and that trend has continued into 2025 and early 2026. Thousands of households each year now receive non-renewal letters even when they have long claim free histories. This pressure is amplified by the fact that Colorado consistently ranks near the top nationally for hail damage claims while wildfire exposure continues to expand well beyond traditional mountain zones.

Carrier behavior has been a major driver of this shift. Several insurers have exited the Colorado homeowners market entirely in recent years while others have reduced new business or imposed stricter underwriting thresholds. American National Group’s withdrawal from homeowners coverage accelerated capacity tightening and larger national carriers such as State Farm, Farmers and Allstate have scaled back availability in higher risk ZIP codes rather than exiting outright. The result for homeowners is fewer renewal offers and more mid-term cancellations tied to inspections and property condition. Many homeowners are now forced to shop for replacement coverage just to avoid a lapse that could violate mortgage requirements. In mountain and foothill communities, non-renewal rates are significantly higher than the statewide average and cancellation notices are now a routine part of the insurance cycle rather than an exception.

Looking ahead through the rest of 2026 homeowners should expect underwriting scrutiny to remain elevated. Insurers are leaning more heavily on property specific risk scoring mitigation verification and tighter underwriting rules when deciding whether to renew or cancel a policy. Higher deductibles increased documentation requests and shorter response timelines are becoming standard especially in wildfire exposed regions and rural corridors. While Colorado is introducing more transparency around risk modeling and rate justification these changes are unlikely to ease availability challenges in the near term. For many homeowners this means preparing well before renewal. It also means understanding how underwriting decisions are made and being ready for the possibility of a non-renewal even when nothing about the home appears to have changed.

Contact Your Insurer Immediately

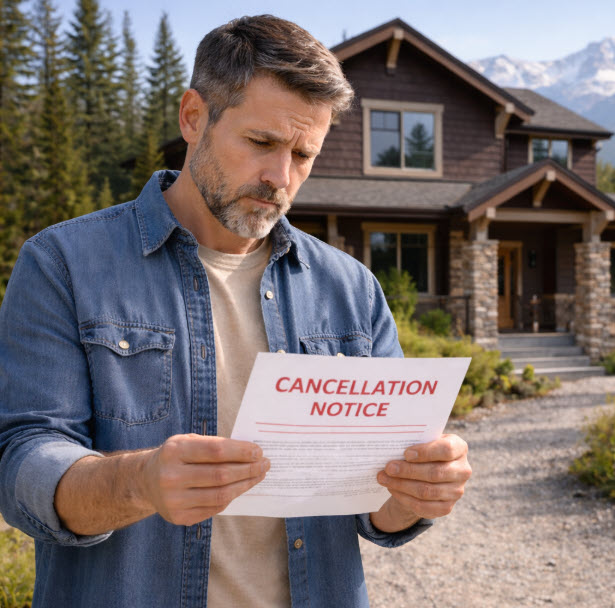

If you receive a homeowners insurance cancellation notice or non-renewal letter the first step is to contact your insurer and confirm exactly why the decision was made. Most cancellations stem from identifiable issues such as missed payments, updated underwriting guidelines, property condition concerns or increased location-based risk. In Colorado this often includes wildfire exposure in foothill and mountain areas along with severe hail risk on the Front Range. Insurers commonly use satellite imagery along with third party data and automated risk scoring to identify issues like aging roofs overgrown vegetation or nearby hazards. In some situations, coverage can continue if corrective steps are taken quickly which makes understanding the precise reason for the cancellation critically important.

Depending on the circumstances, reinstatement may still be possible if you act promptly. Some insurers will reinstate coverage after overdue premiums are paid, documentation of completed or scheduled repairs is provided. Also risk mitigation steps such as defensible space or fire-resistant upgrades are implemented can help. Others may require an updated inspection to confirm that previously identified issues have been addressed. If reinstatement is approved always request written confirmation so there is no uncertainty about coverage status. If you believe your policy was canceled without proper notice or a valid reason you also have the option to file a complaint with the Colorado Division of Insurance through DORA. Even while a review is pending it is important to avoid a coverage gap by exploring replacement policy options as soon as possible.

Shop for New Coverage

If your homeowners insurance has been canceled or non-renewed securing replacement coverage should be a top priority. A lapse in coverage can leave you financially exposed and may place you out of compliance with your mortgage requirements. In Colorado availability now varies widely by location and risk profile. Homes in higher risk wildfire areas often require excess and surplus coverage, especially if they are located in mountain or foothill zones with limited standard carrier appetite. That said standard carrier coverage may still be possible if your home has meaningful upgrades such as a newer roof fire resistant materials documented mitigation work or defensible space. In many cases your strongest chance of placement comes from a bundled policy structure such as home and auto coverage together since carriers are more willing to commit when the overall account is broader.

When shopping for new homeowners insurance it is important to be prepared and patient. Excess and surplus carriers operate differently than standard insurers and underwriting can take longer with quote timelines ranging from several days up to two weeks depending on inspections documentation and carrier review. You should be ready to provide detailed property information photos roof age/ composite, fire mitigation details, and prior loss history upfront to avoid delays. It is also important to look beyond price alone and understand differences in wildfire and hail coverage deductibles and replacement cost terms. While the process can feel slower than it once did taking a thorough and organized approach gives you the best chance to secure stable coverage and avoid repeated cancellations in the future.

Consider the Colorado FAIR Plan (Last Resort)

If you are unable to secure homeowners insurance after a cancellation or non-renewal the Colorado FAIR Plan may be a last resort option. This state backed program provides basic property coverage for homeowners denied insurance due to wildfire risk high claims history or location in a high-risk area. It can help prevent a total lapse in coverage which is important for mortgage compliance, but it is not a replacement for a standard homeowners policy. FAIR Plan coverage is more limited and typically comes with higher premiums and fewer protections such as personal liability or additional living expenses. Because rates reflect elevated risk homeowners should review all private market options first since standard or excess market policies often offer broader coverage when mitigation or property upgrades are in place.

Even If You Can Get Insured Still Implement Risk Mitigation Measures

Reducing risk at your property plays a major role in whether you can secure homeowners insurance in 2026 and how much you ultimately pay. Underwriters now place heavy emphasis on a home’s physical condition with the roof being one of the most important factors they review. A newer roof especially one made with hail resistant or fire-resistant materials can significantly improve eligibility and pricing while older roofs are one of the most common reasons for cancellations non-renewals and declined quotes. Insurers also evaluate how well a home is protected against wildfire hail wind and water damage which means upgrades like reinforced windows improved drainage modern electrical systems and updated plumbing all carry real weight during underwriting.

In wildfire prone areas risk mitigation has become essential rather than optional. Creating defensible space by clearing dry vegetation trimming trees away from structures and using fire resistant landscaping can materially improve how a property is viewed by insurers. Additional improvements such as ember resistant vents fire resistant siding and interior sprinkler systems can further strengthen eligibility and sometimes unlock better terms. Even if you are currently insured these measures help reduce the chance of future non-renewal and put you in a stronger position if you need to shop for coverage later. In today’s market proactive mitigation is one of the most effective ways to protect both your home and your ability to keep it insured long term.

Stay Calm & Get Insured

Receiving a non-renewal or cancellation notice can be stressful but there are still paths forward to keep your home protected. The most important step is taking action early whether that means confirming reinstatement options with your current carrier preparing to shop for new coverage or addressing mitigation items that affect eligibility. While some private insurers continue to scale back in Colorado alternatives still exist including specialty markets and the Colorado FAIR Plan if nothing else is available. Castle Rock Insurance and its partners work with homeowners across a wide range of risk profiles to help navigate these challenges. If you received a non-renewal notice for your homeowners insurance, make sure to reach out to us today.